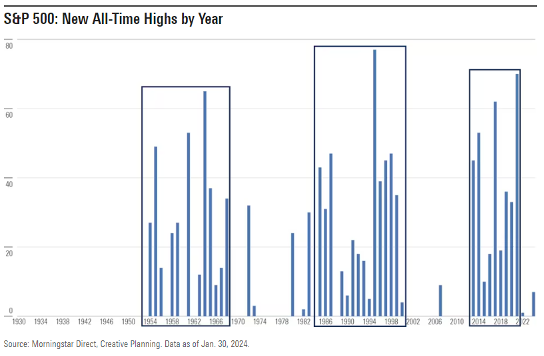

PRESIDENTIAL ELECTION

Regardless of your politics, this year’s presidential election is creating some concern. However, when we look at past election years, the stock market has performed relatively well no matter which party controls the White House or Congress. It is also reassuring that the stock market rose in 20 of the last 24 election years.1 The Wall Street Journal published an article in early September about this topic with essentially the same takeaway. While our analysts are keenly aware of current issues, they continually look ahead seeking to own high-quality companies because, in our experience, this is the key to building wealth over time.

INTEREST RATES

Interest rates have slowly inched downward over the past two years in anticipation of Federal Reserve rate cuts. These rate cuts were confirmed at an August 2024 meeting where the Federal Reserve Chairman, Jerome Powell, stated, “The time has come for policy to adjust.” Lower rates should help increase home and automobile purchases, create an uptick in commercial construction projects, position businesses in certain sectors to thrive, and improve consumer confidence.

FEARS OF A RECESSION

Profits are still growing, overall, but results are mixed across sectors and industries. For instance, insurance, aggregates, and some high-tech pockets are performing well while industrials and banking are flat.

Our research team continues to visit our holdings’ headquarters and monitor them, attend conferences to discover new opportunities, and engage with customers and suppliers at industry trade shows. We still see encouraging signs at the company level, including dividend growth, stock buybacks, and mergers and acquisitions. Because of this shareholder value creation, coupled with increasing profits, we remain bullish on stocks since stock prices tend to follow earnings over time.

AI

Increasing enthusiasm surrounding AI and considerable capital investments in its infrastructure have helped propel the positive stock market returns this year. At the same time, we are still in the very early stages of this technology and no one knows what the future holds. In fact, there are many similarities to the excitement of the dot-com era.

As businesses strive to constantly improve, AI should help them to mine, process, and analyze data faster than ever before. While it remains to be seen how AI will take shape, we expect that many of our holdings should benefit from increased AI investment due to the services and technologies they provide.

LOOKING AHEAD

To reiterate, rising corporate profits typically lead to rising stock prices. These earnings are the result of hard work, ingenuity, and the compounding of knowledge and capital—not politics. Throughout Fenimore’s half-century in business, it has paid to believe in corporate America.

We will continue to follow our market-tested investment approach, identifying what we deem to be high-quality companies, purchasing shares in them if they are available at appealing prices, and, ideally, holding them for many years as they grow profits. When we execute our plan effectively, we expect healthy returns over time, regardless of the temporary challenges experienced along the way.

STAY CONNECTED

Please do not hesitate to connect with us about your investments and financial goals at our Cobleskill or Albany office. You can also contact us from the comfort of your home by calling 800.932.3271 or emailing us at info@fenimoreasset.com.

Thank you for your confidence in us.

Sincerely,

John D. Fox, CFA®

CHIEF INVESTMENT OFFICER

1 FactSet as of 8/31/2024