Letter From Cobleskill: Spring 2022

Letter From Cobleskill: Spring 2022

-

Insert Text here

Dear Fellow Shareholder,

As I write this, our thoughts and hearts are with the people of Ukraine. May our world leaders soon find a path to peace.

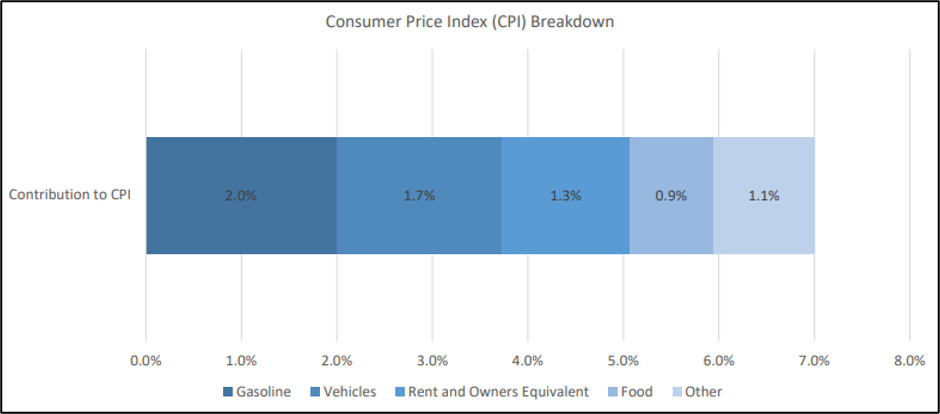

After a terrific 2021, the stock market has dropped 10% to 20%, depending on the index, since the beginning of 2022.1 The war in Ukraine has certainly played a role, but that is not the only reason in our view. As we entered the year, stock valuations were stretched and this left stock prices at an all-time high and susceptible to decline. Additionally, the inflation that began gripping our nation late last year has proven to be more firmly entrenched than originally believed.

Inflation has led to decreased consumer spending as higher prices on essentials like energy and groceries are forcing many people to cut back on discretionary spending (such as vacations and entertainment). As the first quarter ended, the Federal Reserve was beginning the gradual and delicate balancing act of trying to raise interest rates enough to further slow spending — and inflation — but not so much as to trigger a recession.

-

Insert Image here

As long-term investors, it is always helpful to remember that stock market downturns are part of the experience. I have been at Fenimore for 26 years and in every one of those years but one, the market had a decline of 5% or more at least once during the year. This is a normal part of stock investing and, while some uncertainty lies ahead, we see no reason for panic.

First, the current downturn started when our economy was in a position of great strength with consumer spending and corporate earnings at record highs. This is helping to cushion the fall. In addition, interest rates, while rising, are still low by historical standards.

At the same time, what reassures us the most about the days ahead is what our research analysts are hearing directly from the individual companies in which we invest. In recent months, we have met with dozens of businesses to discuss the health of their operations and their roadmaps to growth. While there are certainly challenges (global supply chain problems and elevated transportation prices will be with us the rest of the year), these executives are far from pessimistic.

They intend to grow, reinvest, make acquisitions, and return profits to shareholders in the form of stock buybacks and increased dividends — maybe not to the degree we thought possible three months ago, but certainly at what we consider healthy levels. Overall, these leaders reported that order backlogs are robust, business remains good, and profit margins, while down, are still expected to allow for growth-related activities. We are confident in the collection of businesses in our funds.

Fenimore continues to invest toward a return to “normal.” This means focusing on quality companies that meet our rigorous standards and have the ability, in our opinion, to weather the challenging times and excel when the environment is better. We have made slight adjustments in the funds with an eye on strengthening positions in well-managed, reasonably-priced businesses that may be experiencing short-term pressures, but that we believe should be stronger three years from now. Similarly, we reduced our stakes in companies whose prices peaked in our view and whose long-term prospects are not as favorable.

A DECADE OF DILIGENT MANAGEMENT

Fenimore is proud to celebrate the 10-year anniversary of our FAM Small Cap Fund (FAMFX). Our team is pleased with the performance we delivered for shareholders over that time while seeking to mitigate risk. Under the direction of Portfolio Managers Andrew Boord and Kevin Gioia, we pursue quality, solidly profitable, and sustainable small-cap companies with long-term growth potential. Congratulations to Andrew and Kevin and the entire investment research team! We also thank everyone who is invested in FAMFX and look forward to the next decade.

LET’S CONNECT

We value our personal connections with shareholders. You can reach us with any questions at 800-932-3271, through our website’s “Contact Us” section, or via info@fenimoreasset.com. Our team also welcomes you to meet with us in either our Albany or Cobleskill location or virtually.

Sincerely,

John D. Fox, CFA

CHIEF EXECUTIVE OFFICER

——

1 FactSet, as of 3/18/2022